Strategy Guide: Grid Strike

Grid Strike (grid_strike) is a Controller in Hummingbot's StrategyV2 framework that automatically places a grid of buy or sell orders within a set price range.

Unlike basic grid strategies, Grid Strike utilizes Executors which dynamically manage each order level with configurable take profit and stop loss settings. This means every position opened by the strategy is automatically monitored and closed according to your risk parameters. It can be configured to move with the market trend —- either up or down -- letting you adapt the strategy to changing market conditions.

This guide explains how the Grid Strike strategy works and helps you decide when to use it. You'll learn how to configure and run the strategyt, as well as the key concepts and how to set it up for trending markets.

Strategy Code: https://github.com/hummingbot/hummingbot/blob/master/controllers/generic/grid_strike.py

Strategy Overview

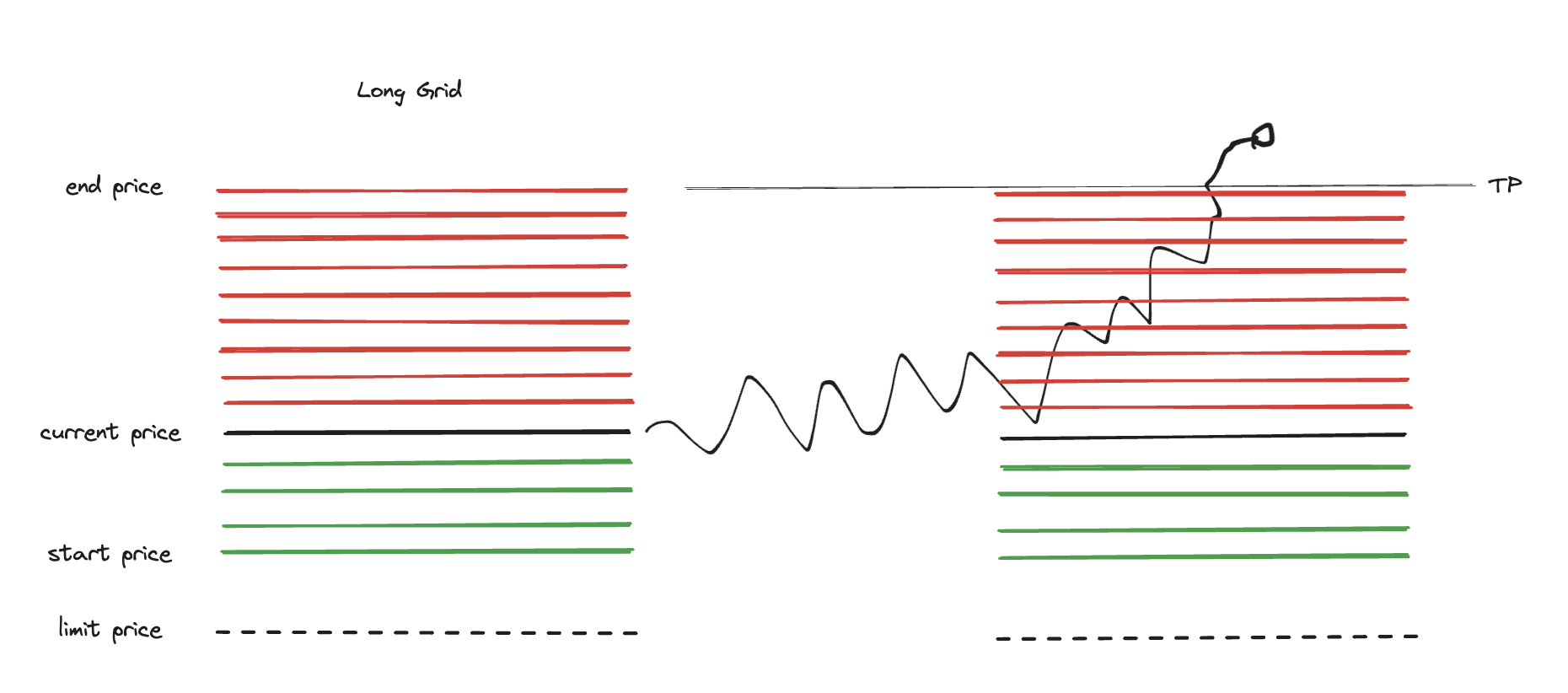

- Grid-based Order Placement: The strategy lets you place either a Long Grid or a Short Grid that places buy/sell orders across a defined price range

- Automated Risk Management: Each side utilizes Grid Executors that automatically manages the risk of each position with configurable take profit, stop loss, and time limits

- Exchange Flexibility: Works on both spot and perpetual exchange connectors, including support for one-way position mode on perp exchanges

- Highly Configurable Can be tailored for various market scenarios (trending up, trending down, or consolidating) or trading objectives (volume, liquidity, P&L, etc) by adjusting price range, order spacing, and other parameters