Creating a Custom Market Making Strategy - Part 5¶

Code: https://gist.github.com/david-hummingbot/f9332923faac2fb5485eb7a80eb0d08d

Video:

Finally, let’s learn how to customize our script by utilizing order book data, leveraging Hummingbot’s ability to synchronously stream real-time Level 2 order book data from multiple exchanges simultaneously.

Dynamic calculation using Bollinger Bands¶

We will improve the last exercise by adding a dynamic calculation of the price ceiling/floor feature based on the Bollinger Bands.

To do so, we will:

- Use the

CandlesFactoryobject that will create an instance of the candles of the trading pair and interval that we want. Is important to notice that we can create as many candles as we want and they are not related to the markets that you define on the class variablemarkets. This is handy for example if you want to trade on KuCoin with the information of Binance. - Once we get the class of the candles, we need to start them. The start will initialize the WebSocket connection to receive the most updated information on the current candle, and also request the historical candles needed to complete the records requested. We are going to do this on the

__init__. - Also we need to add a method to stop the candle when the script is stopped. We can override the method

on_stopwhich let’s us code a custom shutdown when the bot is stopped via the stop command. - To calculate the bounds we are going to create a method that will add the Bollinger Bands using as a value 100 periods and 2 std. Then the upper bound will be

price_ceilingand the lower bound will beprice_floor.

Now, let’s implement the solution, extending the same file as the last example: quickstart_script_2.py.

Let's code!¶

First, we will create an candle instance:

import logging

from decimal import Decimal

from typing import List, Dict

import pandas as pd

import pandas_ta as ta # noqa: F401

from hummingbot.core.data_type.common import OrderType, PriceType, TradeType

from hummingbot.core.data_type.order_candidate import OrderCandidate

from hummingbot.core.event.events import OrderFilledEvent

from hummingbot.data_feed.candles_feed.candles_factory import CandlesFactory, CandlesConfig

from hummingbot.strategy.script_strategy_base import ScriptStrategyBase

class QuickstartScript2(ScriptStrategyBase):

bid_spread = 0.008

ask_spread = 0.008

order_refresh_time = 15

order_amount = 0.01

create_timestamp = 0

trading_pair = "ETH-USDT"

exchange = "binance_paper_trade"

# Here you can use for example the LastTrade price to use in your strategy

price_source = PriceType.MidPrice

price_ceiling = 1700

price_floor = 1600

candles_config = CandlesConfig(connector="binance",

trading_pair="ETH-USDT",

interval="1m",

max_records=500)

eth_1m_candles = CandlesFactory.get_candle(candles_config)

markets = {exchange: {trading_pair}}

- We import the

CandlesFactory&CandlesConfigclass and call theget_candlemethod to create a candle instance in the variableeth_1m_candles. - Note that we are importing

pandas_ta, a library that we will use to generate technical indicators from the candle data. - While we still define initial values for

price_ceilingandprice_floor, we will override them later in theon_tickmethod.

Add functions that override the __init__ and on_close methods:

def __init__(self, connectors: Dict[str, ConnectorBase]):

# Is necessary to start the Candles Feed.

super().__init__(connectors)

self.eth_1m_candles.start()

The method above starts collecting data when the script starts.

def on_stop(self):

"""

Without this functionality, the network iterator will continue running forever after stopping the strategy

That's why is necessary to introduce this new feature to make a custom stop with the strategy.

:return:

"""

self.eth_1m_candles.stop()

The method above stops collecting data when the user runs the stop command.

calculate_pricing_ceiling_floor¶

Add a method that uses the data in eth_1m_candles to calculate moving price ceiling/floor using Bollinger Bands and update the values of the price_ceiling and price_floor.

def calculate_price_ceiling_floor(self):

candles_df = self.eth_1m_candles.candles_df

candles_df.ta.bbands(length=100, std=2, append=True)

last_row = candles_df.iloc[-1]

self.price_ceiling = last_row['BBU_100_2.0'].item()

self.price_floor = last_row['BBL_100_2.0'].item()

Now, let’s add it to on_tick:

def on_tick(self):

if self.create_timestamp <= self.current_timestamp and self.eth_1m_candles.is_ready:

self.cancel_all_orders()

self.calculate_price_ceiling_floor()

proposal: List[OrderCandidate] = self.create_proposal()

proposal_filtered = self.apply_price_ceiling_floor_filter(proposal)

proposal_adjusted: List[OrderCandidate] = self.adjust_proposal_to_budget(proposal_filtered)

self.place_orders(proposal_adjusted)

self.create_timestamp = self.order_refresh_time + self.current_timestamp

- We are adding a new condition that will block the execution if the candles are not ready.

- Then we are adding the method

calculate_price_ceiling_floorand the implementation is accessing to the dataframe of the Candles object by using the methodself.eth_1m_candles.candles_df - Lastly, we are getting the last row and assigning the upper and lower bound to

price_ceilingandprice_floor

Tip

Check out the pandas-ta documentation to learn how to generate other types of technical indicators.

Custom status¶

Before we run the script, let’s improve the status command and show the candles data, as well as the current values for the price_ceiling and price_floor.

def format_status(self) -> str:

if not self.ready_to_trade:

return "Market connectors are not ready."

lines = []

mid_price = self.connectors[self.exchange].get_price_by_type(self.trading_pair, PriceType.MidPrice)

best_ask = self.connectors[self.exchange].get_price_by_type(self.trading_pair, PriceType.BestAsk)

best_bid = self.connectors[self.exchange].get_price_by_type(self.trading_pair, PriceType.BestBid)

last_trade_price = self.connectors[self.exchange].get_price_by_type(self.trading_pair, PriceType.LastTrade)

custom_format_status = f"""

| Mid price: {mid_price:.2f}| Last trade price: {last_trade_price:.2f}

| Best ask: {best_ask:.2f} | Best bid: {best_bid:.2f}

| Price ceiling {self.price_ceiling:.2f} | Price floor {self.price_floor:.2f}

"""

lines.extend([custom_format_status])

if self.eth_1m_candles.is_ready:

lines.extend([

"\n############################################ Market Data ############################################\n"])

candles_df = self.eth_1m_candles.candles_df

# Let's add some technical indicators

candles_df.ta.bbands(length=100, std=2, append=True)

candles_df["timestamp"] = pd.to_datetime(candles_df["timestamp"], unit="ms")

lines.extend([f"Candles: {self.eth_1m_candles.name} | Interval: {self.eth_1m_candles.interval}\n"])

lines.extend([" " + line for line in candles_df.tail().to_string(index=False).split("\n")])

lines.extend(["\n-----------------------------------------------------------------------------------------------------------\n"])

else:

lines.extend(["", " No data collected."])

return "\n".join(lines)

- We are using the list approach to add strings and then show all of them

- First, we are adding to our original text the price ceiling and price floor

- Then we are logging the information of the candles.

- Check that when you run the code, the last candle is updated in real-time ;)

Running the script¶

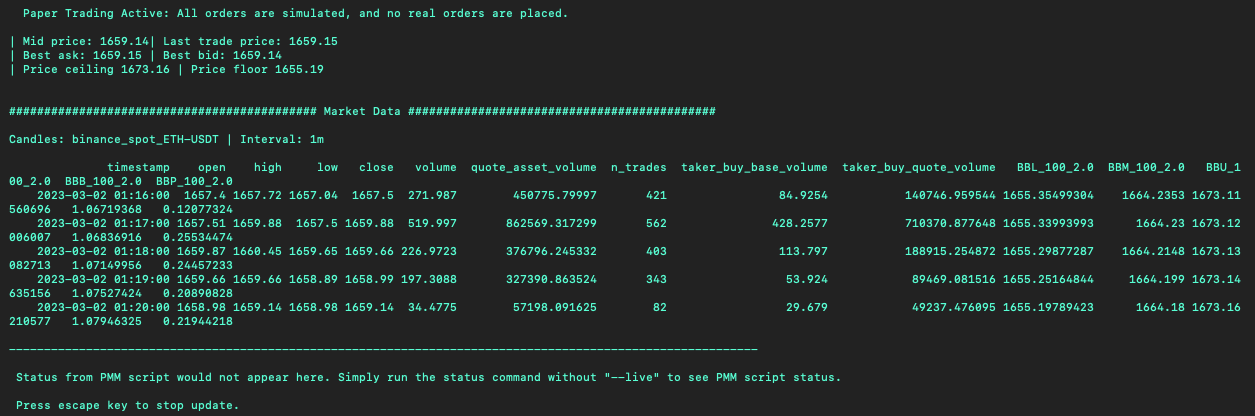

Run the script with start again.

After it’s running, run status --live to see your dynamic price ceiling/floor along with the candles data streaming in real-time!

You can display any variable you want here, so use it to analyze what is happening with your bot.

Debugging scripts¶

Watch this video to learn how to debug Scripts at runtime with the PyCharm IDE:

Congratulations on successfully building your own custom market making script!

If you’d like to learn more about how to build custom strategies using Hummingbot, check out Botcamp!